Proxy Voting 101 – White Paper

Executive Summary

- Shareholders are the owners of companies and have the right to vote each year on proposals governing them. This fact used to be well-known, but over the last century many Americans have forgotten that shares come with voting rights attached.

- The rise of passive investing has transferred legal ownership of shares of public companies from individual investors to the asset managers who offer them index funds.

- Recently, thanks to their embrace of stakeholder capitalism, large asset managers have begun to use the power of the proxy vote to advance social and political causes. This means that they are using their clients’ money to support other peoples’ interests.

- Strive aims to restore the proxy vote’s original purpose and use it as it was always intended: to exercise ownership to maximize shareholder value.

Introduction

To own a share of a corporation is to own a piece of it and have a say in what it does. Every year a company’s owners have the chance to use their say at its shareholder meeting, where they elect members of its board of directors and approve executives’ pay. They also vote on proposals from management and shareholders. Instead of traveling, shareholders usually vote online, by phone, or by mail: voting by proxy. Companies mail out proxy statements describing upcoming proposals and often attach proxy cards shareholders can send back with their votes.[1]

For most of US corporate history, the proxy vote was a formality; corporate executives called the shots. But over the last couple decades shareholders have awoken to their power. Sometimes they use that power for good, fixing inefficiencies in a company or reining in bad behavior from its managers. More recently, activists have realized they can use the proxy ballot to pass shareholder proposals meant to advance social causes. This paper explains where proxy voting came from and how it got derailed by politics.

How shareholders lost their voice

The story starts in 1600, when the ancestor of the modern corporation was born. To finance trade with Asia, English merchants formed a joint-stock company called the East India Company, allowing a broad pool of investors to own small shares of the enterprise. Upon completing a voyage, the company would liquidate itself then distribute its assets and profits among shareholders in divisions, now called dividends. It would re-form with new shareholders for the next journey. After realizing this process was wasteful, the English East India Company turned itself into a permanent legal entity with its own assets and rights—it incorporated.[2]

The efficiency of the stock-based corporate structure allowed the English corporation and the rival Dutch East India Company to dominate the known world. The English company raised armies and conquered India; the Dutch one colonized Indonesia. The same corporate form flourished in America and became even more potent after the United States won independence.

US corporations originally followed the one-person one-vote model of their European predecessors; shareholder democracy mirrored actual democracy. But Alexander Hamilton and others argued owners of more shares deserved more say. By the late 1800s, US corporations had transitioned entirely to one-share one-vote, giving owners with greater stakes greater control, incentivizing them to invest more but drowning out everyday investors.

European and American capitalism began to diverge. The European focus on democracy eventually broadened into modern stakeholder capitalism, the view that all people affected by a corporation’s actions deserve a say in its decisions, not just shareholders. The American focus on efficiency eventually narrowed into the belief that corporations’ only duty was to maximize shareholder profit. Americans first forgot they had believed every shareholder deserved a say, then gradually forgot they had ever believed any shareholder deserved a say.

By the 1900s, all US shareholders were powerless. As the United States expanded west and its territories grew, so did its corporations. They began hiring professional executives, creating the modern corporation, run by a managerial class separate from its owners that may not always have their interests at heart. This problem became known as the separation of ownership from control. Much of corporate law—including executives’ duty to maximize shareholder profit and shareholders’ “say on pay” vote on executive compensation—is aimed at solving it.

Mismanagement and fraud contributed to the 1929 market crash and the Great Depression, so in 1934 Congress created the Securities and Exchange Commission to protect shareholders. The SEC was charged with regulating proxy votes; in 1942 it required corporations to publish shareholder proposals in proxy statements, but these had become formalities. From the 1930s through 50s, a few shareholders known as “corporate gadflies” would attend annual meetings, make proposals, and act like owners treating executives as employees, but managers viewed them as amusing novelties.[3]

Though these early shareholder activists’ proposals were rarely adopted, they kept the notion that shareholders were owners on life-support. But most Americans forgot that owning a share of a corporation entails having a say in what it does; they came to believe a share only entitles one to part of a company’s profits. That opened the door for large asset managers to replace them as owners and take their say.

Passive investing gives the proxy vote to asset managers

The coup was unintentional. Passive investing was born out of a desire to save regular investors money, but it accidentally deprived them of the right to vote their shares. That power ended up in the hands of the asset managers who offer index funds.

Passive investing was the brainchild of Jack Bogle. His family had lost everything in the 1929 crash; Bogle grew up believing the financial system was rigged. He realized that thanks to compound interest, even a seemingly small management fee of 1 or 2 percent would, over decades, transfer vast wealth from the pockets of clients to their financial advisors. He dedicated his career to lowering those fees.

His solution was the index fund. At the time, virtually every investor tried to beat the market by actively picking stocks. Bogle learned of an academic theory called the efficient markets hypothesis, which held that the market quickly prices in all public information, meaning few can beat it in the long run. This theory recommended skipping stock-picking and investing in an index reflecting the market itself, protecting investors from volatility and allowing lower fees because no research was required. In 1975 Bogle founded a firm called Vanguard to put his ideas into practice.

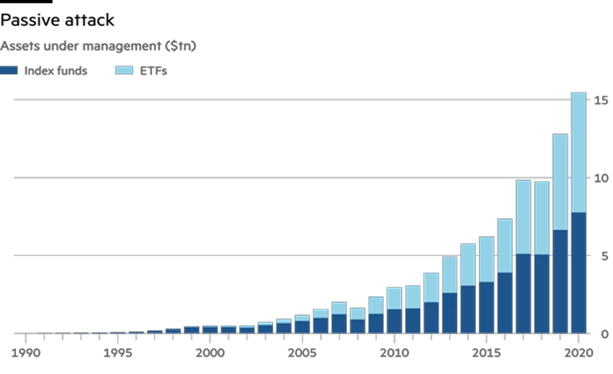

Over the next fifty years, passive investing gradually took over the financial world.

Source: Robin Wigglesworth 2021 “Global passive assets hit $15tn as ETF boom heats up” Financial Times/FT.com 10 May. Used under license from the Financial Times. All rights reserved.

Source: Robin Wigglesworth 2021 “Global passive assets hit $15tn as ETF boom heats up” Financial Times/FT.com 10 May. Used under license from the Financial Times. All rights reserved.

From 1996 to 2020, most active funds charged a fee of almost 1%, while index funds outperformed them and charged only .17%.[4] Financially, passive investing has been a resounding success for investors.

But it came at the cost of their shareholder vote. Investors may think they own shares of the companies in an index; in actuality, they own shares of funds that themselves own shares of those companies. The middlemen who offer these index funds are now the legal owners of public corporations. Today, thanks to passive investing, the three largest asset managers alone—BlackRock, Vanguard, and State Street—own over 22% of the shares of most public companies.[5]

This new problem of corporate structure is called the separation of ownership from ownership.[6] When capital owners signed up for passive investing, they gave their shareholder vote to fund providers like the Big Three, keeping nothing except the right to profit. By the time the index fund became popular, shareholders had forgotten shares came with voting rights attached. Asset managers had largely forgotten about the proxy vote too; for years their power lay dormant. Then they gradually awoke to the fact that they owned all the public companies in America.

Asset managers become activists

Corporate gadflies kept the notion that shareholders were owners alive through the middle of the 20th century, and by the end of it hedge fund activists called corporate raiders realized they could use the proxy vote to manufacture a profit. Investors like Carl Icahn would buy large stakes in a public company, threaten to strip its assets or replace its leaders, then sell their shares back to the company above market price to spare it—greenmail.[7] Raiders would often partner with asset managers to control the proxy vote, opening their eyes to their own voting power.

After executive fraud bankrupted Enron in 2001 and cost shareholders $74 billion,[8] the SEC effectively required asset managers to cast their proxy votes, believing shareholder governance would prevent mismanagement. Initially, they had little interest in overseeing the many corporations in their portfolios. Governance was time-consuming, costly, and usually produced no direct return. Enter proxy advisory firms Institutional Shareholder Services and Glass-Lewis: asset managers outsourced governance responsibility to them.

By that time, corporate raiders had been defanged through legal tricks and regulation, so hedge fund activists used their proxy vote to profit by improving the companies they owned.[9] History briefly came full circle and the shareholder vote fulfilled its original purpose. Shareholder activism became known as a valuable tool to improve a business. That was until social activists realized the proxy vote could be used to compel corporations to change the world.

Political shareholder proposals had existed for decades, but they never had much success. After hedge fund activists, passive investing giants, and proxy advisors restored the power of the proxy vote, social activists merely had to team up with those institutions to finally give their proposals teeth. The 2008 crisis gave them the opportunity. After some soured on shareholder capitalism’s profit focus, European stakeholder capitalism began to gain sway in America. It was given voice through the ESG movement, which advanced social concerns in the guise of having companies focus on environmental, social, and governance risk factors.

The shift accelerated in 2018, when BlackRock chairman Larry Fink took stakeholder capitalism’s side in his annual letter to America’s CEOs. He began by saying that with “many governments failing to prepare for the future… society increasingly is turning to the private sector and asking that companies respond to broader societal challenges.” He argued that fiduciary duty to its index investors required BlackRock to engage with portfolio companies and vote on policies addressing climate change, workforce racial and gender diversity, and other ESG causes.[10]

The dominos fell quickly after that. In the previous decade, average support for environmental and social shareholder proposals had steadily risen from around 10% to 20%; in the two years following Fink’s letter, support spiked to 30%.[11] In 2019, the Business Roundtable, a leading business lobbyist association, released a new “Statement on the Purpose of a Corporation” signed by the CEOs of nearly 200 major companies. The sub header summed it up: “Updated Statement Moves Away from Shareholder Primacy, Includes Commitment to All Stakeholders.”[12] Support for environmental and social shareholder proposals further surged after the racial reckoning in the summer of 2020.[13]

Activists began using the proxy ballot to pass whatever policies the political one could not. New tailwinds lifted them. ISS and Glass-Lewis were acquired by foreign owners with even greater commitments to stakeholder capitalism. Under the Biden Administration, the SEC issued guidelines empowering shareholders to make proposals meant to advance social causes. It cited a desire to implement the Paris Accords’ greenhouse gas reduction targets through the private sector.[14] Emission reduction proposals proliferated.

Jack Bogle had never intended index fund providers to replace governments. Shortly after Fink’s letter, a month before Bogle’s death, he wrote an article warning that the Big Three might soon wield “effective control” over the US stock market, saying “I do not believe that such concentration would serve the national interest.”[15]

His last public words were soon proven right. To own a share of a corporation is to have a say in what it does. Passive investing had transferred that right from Americans to asset managers, and they began to use their say whenever they felt governments weren’t managing society well. The proxy vote had replaced politics.

Now we come to the present, when Strive enters the story. Our goal is simple: use the power of ownership to maximize shareholder value. That was how the shareholder vote was used when the first corporations were created four hundred years ago; that was how it was used a decade ago. And that is how Strive intends to use it for our clients today.

[1] “Prepping for Proxy Season: A Primer on Proxy Statements and Shareholders’ Meetings.” FINRA.org, 6 Feb. 2023, https://www.finra.org/investors/insights/proxy-season-primer-proxy-statements-and-shareholder-meetings.

[2] Wood, Bob G. Jr. “The Evolution of Dividend Policy in the Corporation and in Academic Theory.” LSU Historical Dissertations and Theses, 1994, https://doi.org/10.31390/gradschool_disstheses.5705.

[3] Wells, Harwell. “A Long View of Shareholder Power.” Florida Law Review, vol. 67, no. 3, Jan. 2016, pp. 1078-1081, https://scholarship.law.ufl.edu/cgi/viewcontent.cgi?article=1258&context=flr.

[4] Ro, Sam. “Passive Investors Have Saved a Fortune over the Last 25 Years.” Axios, 2 Aug. 2021, https://www.axios.com/2021/08/02/index-fund-investors-saved-357-billion-over-last-25-years.

[5] Potter, Sam. “Blackrock-Led ‘Big Three’ May Forestall Chaos in Stock Markets.” Bloomberg.com, Bloomberg, 20 July 2021, https://www.bloomberg.com/news/articles/2021-07-20/blackrock-led-big-three-may-forestall-chaos-in-stock-markets.

[6] Strine, Leo E. Jr. “Can We Do Better by Ordinary Investors? A Pragmatic Reaction to the Dueling Ideological Mythologists of Corporate Law.” Columbia Law Review, vol. 114, no. 2, pp. 449-502, Mar. 2014, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2421480.

[7] Cole, Robert J. “To the Raided, He’s Icahn the Terror.” The New York Times, 4 June 1988, https://www.nytimes.com/1988/06/04/business/to-the-raided-he-s-icahn-the-terror.html.

[8] Segal, Troy. “Enron Scandal: The Fall of a Wall Street Darling.” Investopedia, 5 Apr. 2023, https://www.investopedia.com/updates/enron-scandal-summary/.

[9] “Why Shareholder Activists Are Set to Leapfrog North American Companies.” Financier Worldwide, Dec. 2015, https://www.financierworldwide.com/why-shareholder-activists-are-set-to-leapfrog-north-american-companies#.ZCxns3bMK38.

[10] Fink, Larry. “A Sense of Purpose.” The Harvard Law School Forum on Corporate Governance, 17 Jan. 2018, https://corpgov.law.harvard.edu/2018/01/17/a-sense-of-purpose/.

[11] Cook, Jackie. “ESG Proxy Resolutions Find More Support in 2019.” Morningstar, Inc., 28 Feb. 2020, https://www.morningstar.com/articles/967699/esg-proxy-resolutions-find-more-support-in-2019.

[12] “Business Roundtable Redefines the Purpose of a Corporation to Promote ‘an Economy That Serves All Americans’.” Business Roundtable, 19 Aug. 2019, https://www.businessroundtable.org/business-roundtable-redefines-the-purpose-of-a-corporation-to-promote-an-economy-that-serves-all-americans.

[13] Kishan, Saijel, et al. “McDonald’s, Meta, Big Banks Face Investor Pressure with Record ESG Proxy Votes.” Bloomberg.com, Bloomberg, 25 Apr. 2022, https://www.bloomberg.com/graphics/2022-esg-proxy-season/.

[14] “Shareholder Proposals: Staff Legal Bulletin No. 14L.” Securities and Exchange Commission, 3 Nov. 2021, https://www.sec.gov/corpfin/staff-legal-bulletin-14l-shareholder-proposals.

[15] Bogle, John C. “Bogle Sounds a Warning on Index Funds.” The Wall Street Journal, Dow Jones & Company, 29 Nov. 2018, https://www.wsj.com/articles/bogle-sounds-a-warning-on-index-funds-1543504551.